2nd Bac - Economy applied to Entrepreneurship

https://www.youtube.com/watch?v=GqeRnxSuLFI&ab_channel=OneMinuteEconomics

Economy applied to Entrepreneurship....

The knowledge about the behavior of variables that explain the environment in which a productive activity takes place is key for the entrepreneur at the moment of choosing and defining the strategy that will allow them to take advantage of opportunities and defend against threats.

Economy of the Market

All people that have needs such as, clothing, education, eating and recreational can be solved through the acquisition of goods and services.

Goods and Services

A GOOD is an object people want that they can touch or hold. A SERVICE is an action that a person does for someone else. Examples: Goods are items you buy, such as food, clothing, toys, furniture, and toothpaste. Services are actions such as haircuts, medical check-ups, mail delivery, car repair, and teaching.

Goods are tangible objects that satisfy people's wants. Services are actions, such as haircuts and car repair, which also satisfy people's wants. A key point to emphasize to young children is that goods and services must be produced - they don't appear magically on store shelves. Similarly, they are produced using scarce productive resources (natural, human, and capital); thus, the goods and services themselves are considered scarce.

Depending on the grade level, it may be appropriate to teach the distinction between consumer goods and capital goods. Consumer goods are the "final" goods purchased by consumers. Capital goods are those used to produce other goods and services (e.g. Tools, equipment, machinery).

The Market

In a market economy, prices are determined by the interaction of consumers and producers in markets. There are three basic types of markets: Goods and Services, Productive Resources, Financial Capital. The prices that are determined in these markets serve as a guide to economic activity. For example, if the relative price of a certain good is high, this means that there is a potential of greater profits. Entrepreneurs have an incentive to divert resources to the production of that good. Eventually, as supplies of the good increase, the price falls, signaling that productive resources should be diverted to the production of other goods or services.

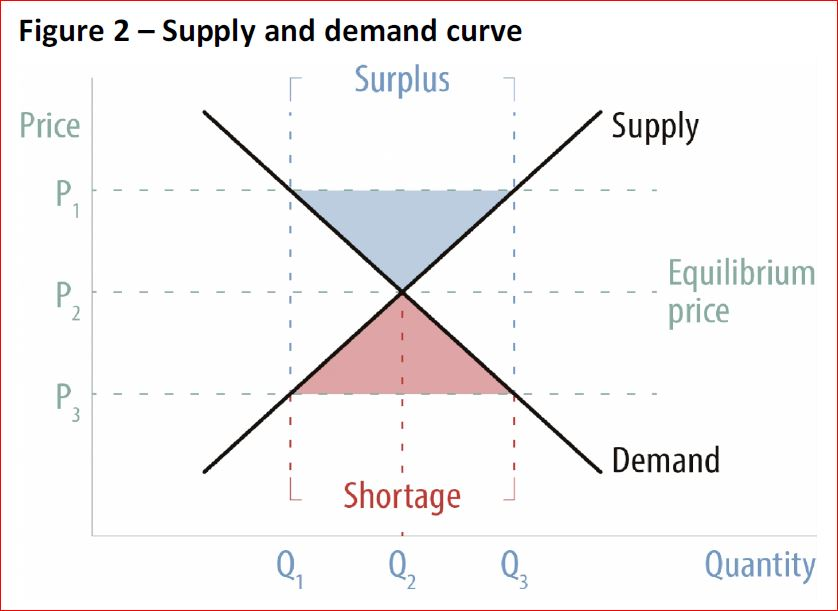

Supply and Demand

A market exists whenever buyers and sellers exchange goods or services. Buyers (consumers) demand goods and services; sellers (producers) supply them. The interaction of buyers and sellers determines market prices. (The market price is also known as the market clearing price or the equilibrium price.) At the market price, the amount consumers want to buy equals the amount producers want to sell. Prices send signals and provide important incentives to both consumers and producers. At higher prices, consumers have an incentive to purchase less, while producers have an incentive to produce more. At lower prices, consumers purchase more, but producers have an incentive to produce less.

Market prices fluctuate as supply and demand change. If other things do not change, an increase in supply or a decrease in demand causes prices to fall. A decrease in supply or an increase in demand causes prices to rise. Many markets are very interrelated, with changes in the price of one good or service leading to changes in the price of other goods and services. (For example, a large, sustained increase in the price of gasoline will decrease the demand for cars with very poor gas mileage.)

https://www.youtube.com/watch?v=kIFBaaPJUO0&ab_channel=JacobClifford

Comments

Post a Comment